Our Advantage

RPC exists to bring the same captive insurance structure used by the industry's largest operators to the best owners in the middle market, saving our members 25% to 35% on year-one premiums, with the opportunity to receive dividends from underwriting profit and investment income earned by the captive.

Members purchase lender-compliant insurance through an institutional captive structure while participating in the financial results of the program they help create.

1. Aggregation & Scale

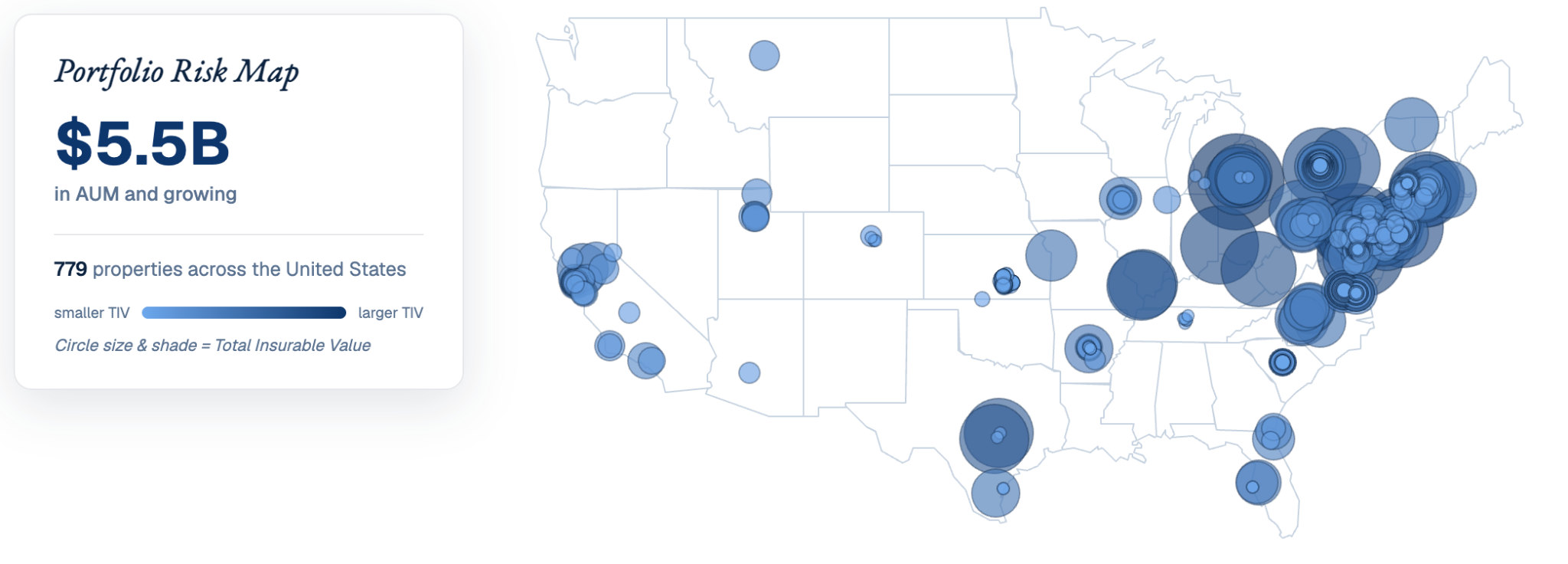

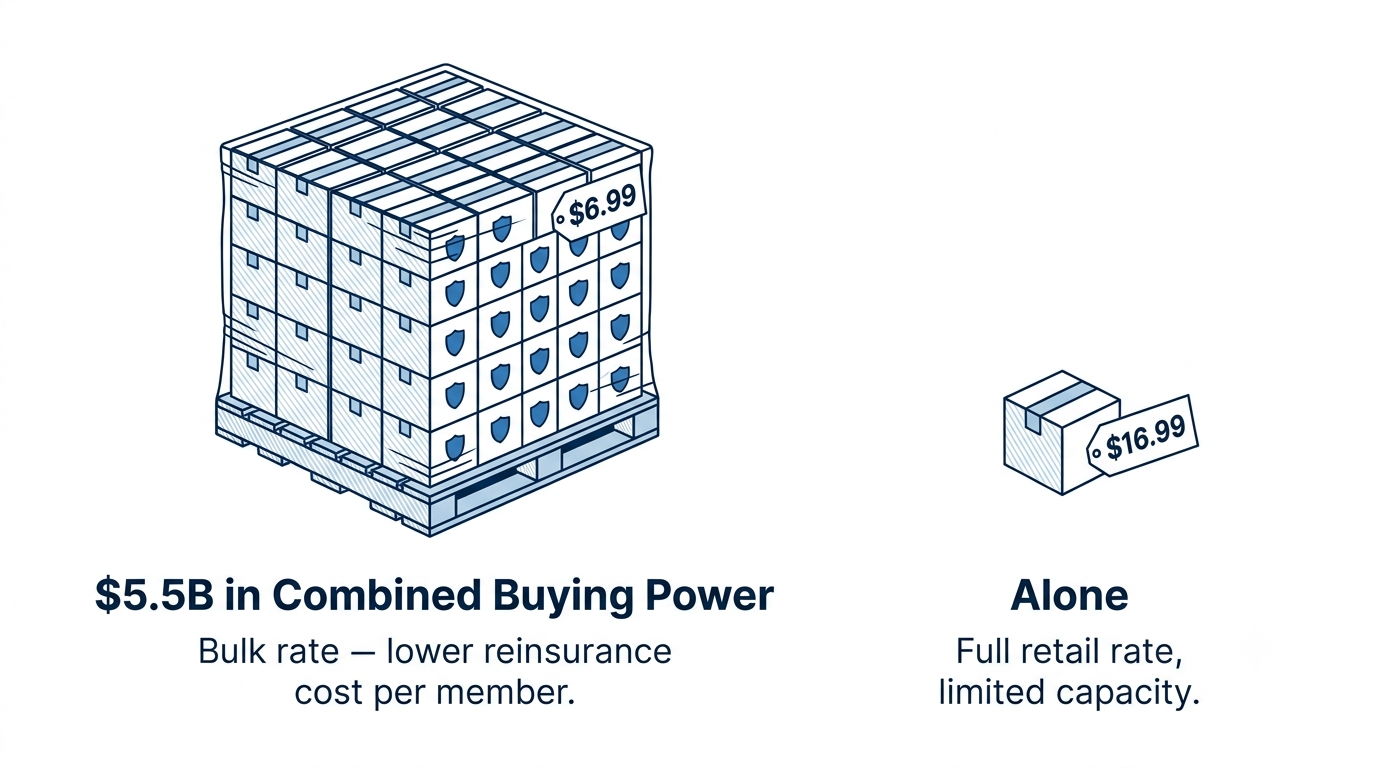

RPC currently represents a $5.5 billion property portfolio across 12 member companies. The captive approaches reinsurance markets and program vendors with the scale, diversification, and spread of risk created by the group, not as a collection of isolated middle-market buyers. RPC is targeting $100 billion in portfolio size in the near future.

Aggregation allows RPC to approach the market with:

- •A larger and more diversified premium base

- •Broader geographic spread

- •Greater asset-level diversification

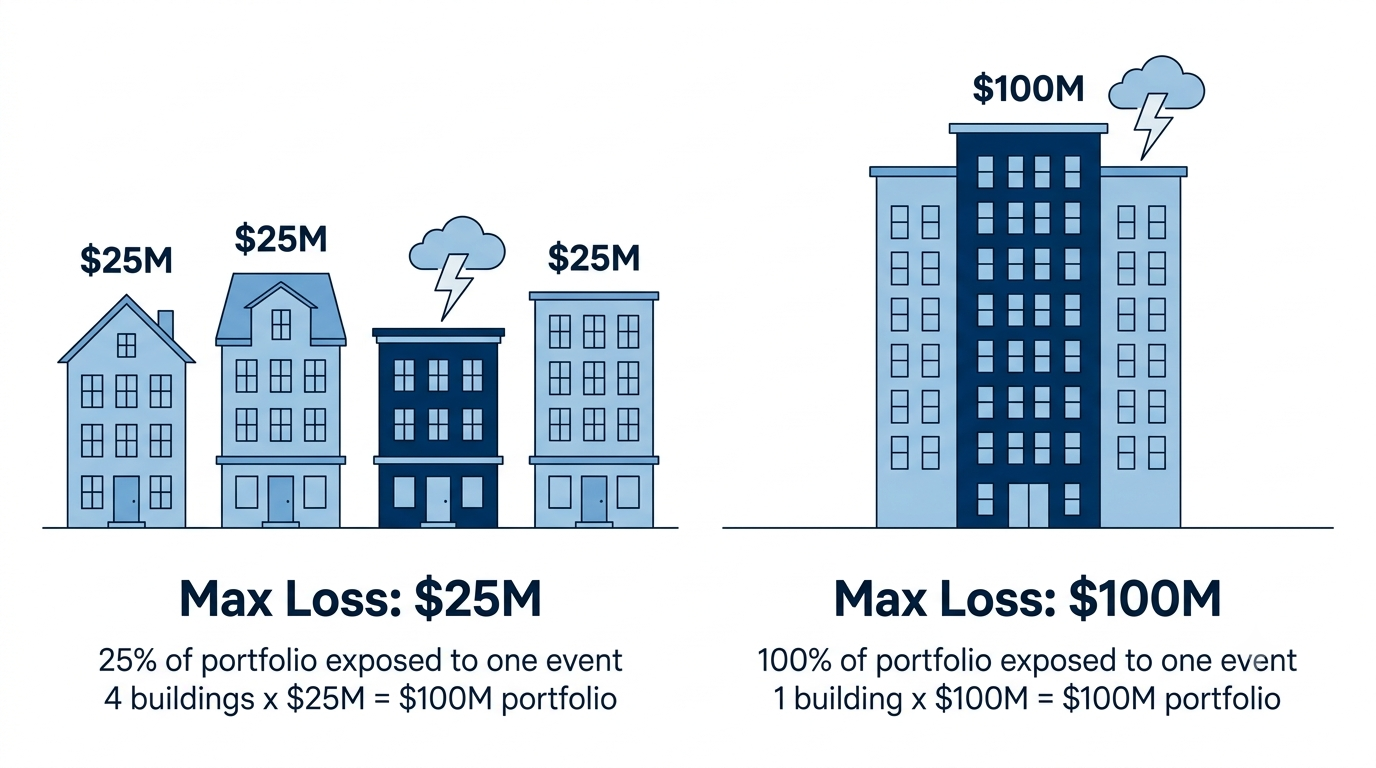

- •Lower concentration in any single operator or property

- •More efficient use of reinsurance capital

- •Stronger purchasing power across program vendors

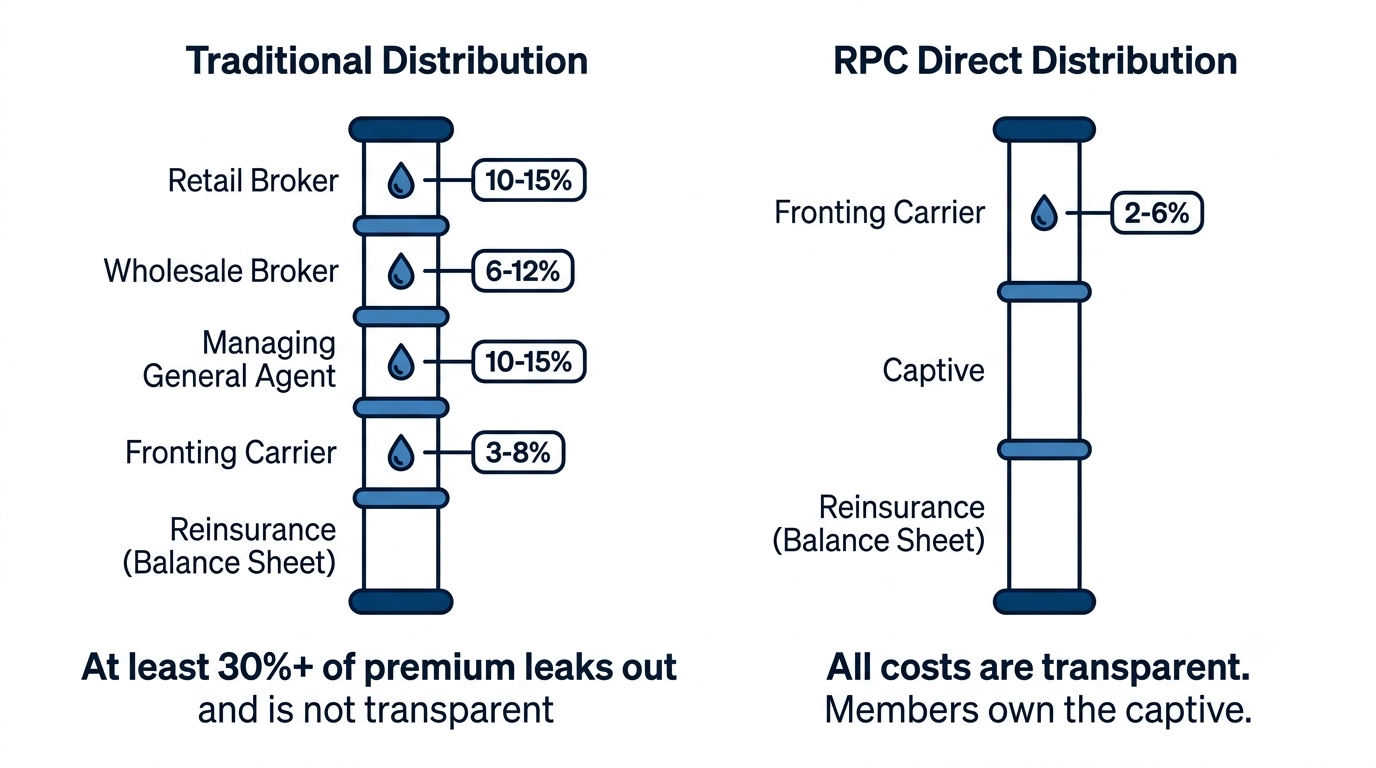

2. Direct Distribution

Before RPC, many of our members were subject to fee leakage of up to 30% through multiple layers of insurance distribution. RPC was constructed from inception to be as efficient as possible: members purchase policies from the program's fronting partner, which then reinsures the agreed captive layer back to RPC and transfers the remaining risk to the program's panel of reinsurers.

The RPC structure is designed to:

- •Reduce redundant distribution layers

- •Align placement decisions with captive performance

- •Allow more premium dollars to support risk, surplus, and potential member dividends

- •Create clearer visibility into program economics

- •Maintain required regulatory, licensing, and fiduciary standards

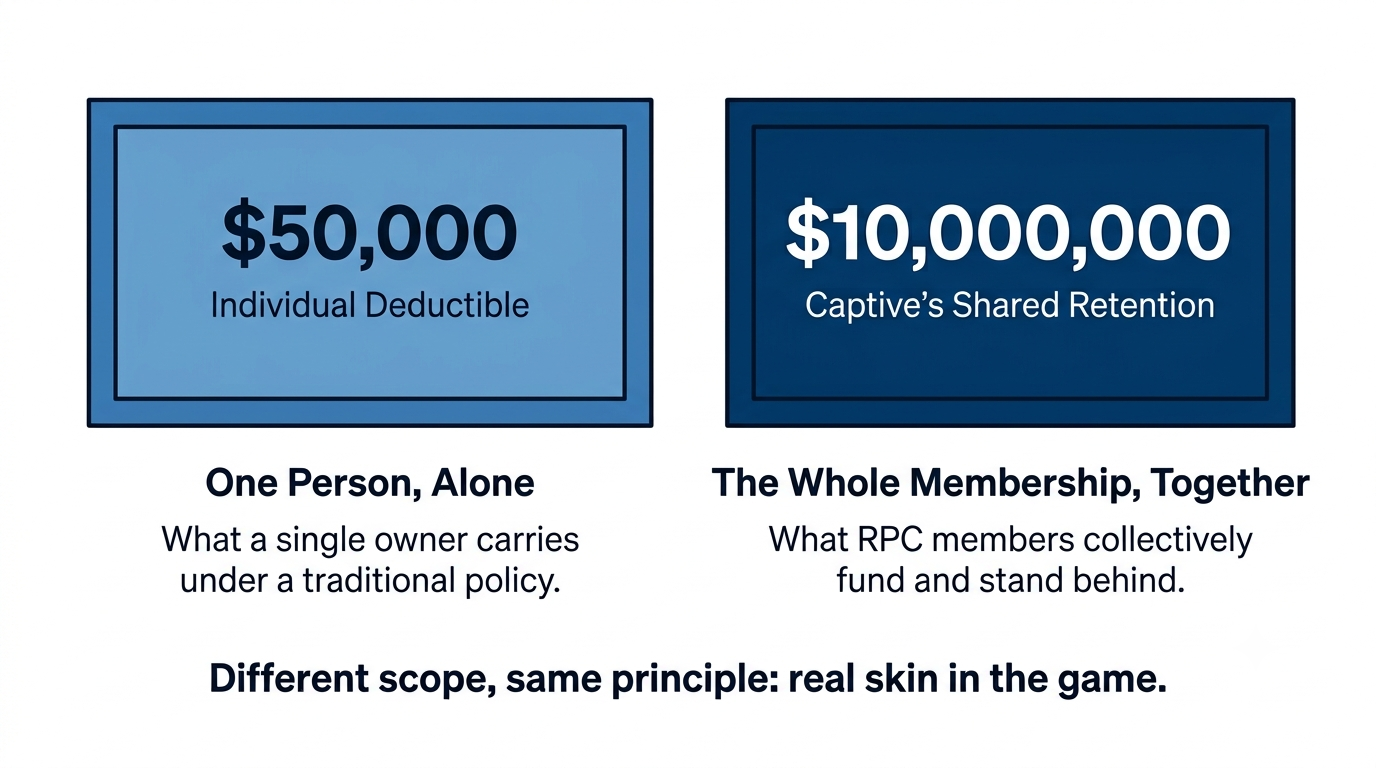

3. Strict Underwriting & Skin in the Game

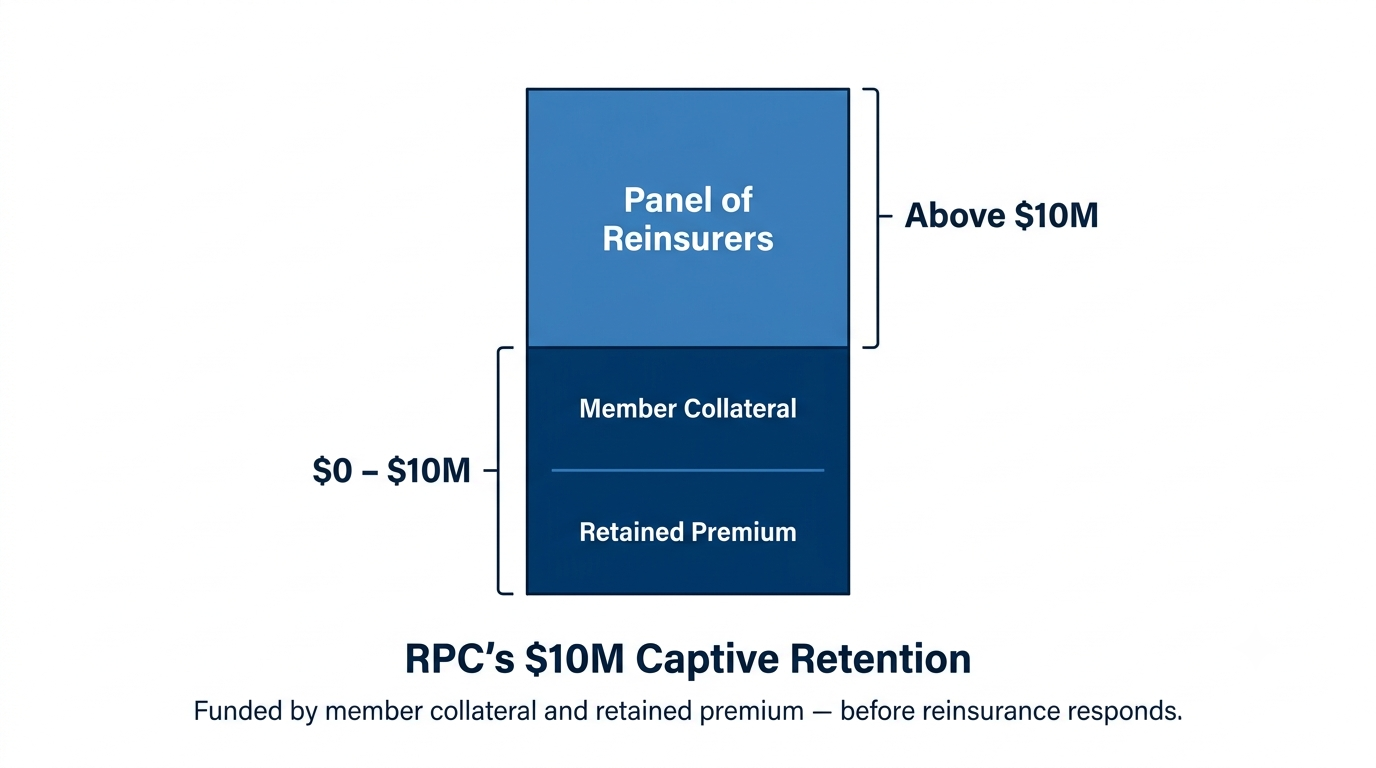

RPC is designed around meaningful risk retention. The captive retains the first $10 million of aggregate member losses before the applicable reinsurance layers respond, funded through member collateral and premium retained within the captive. Membership is intentionally selective: prospective members are expected to demonstrate a portfolio loss ratio below 25%, subject to underwriting review.

Member alignment is created through:

- •Collateral contributed to support the captive retention

- •Premium retained within captive layers

- •Selective underwriting and historical loss-performance requirements

- •Potential dividends tied to underwriting results

- •Voting and governance rights regarding admission of future members

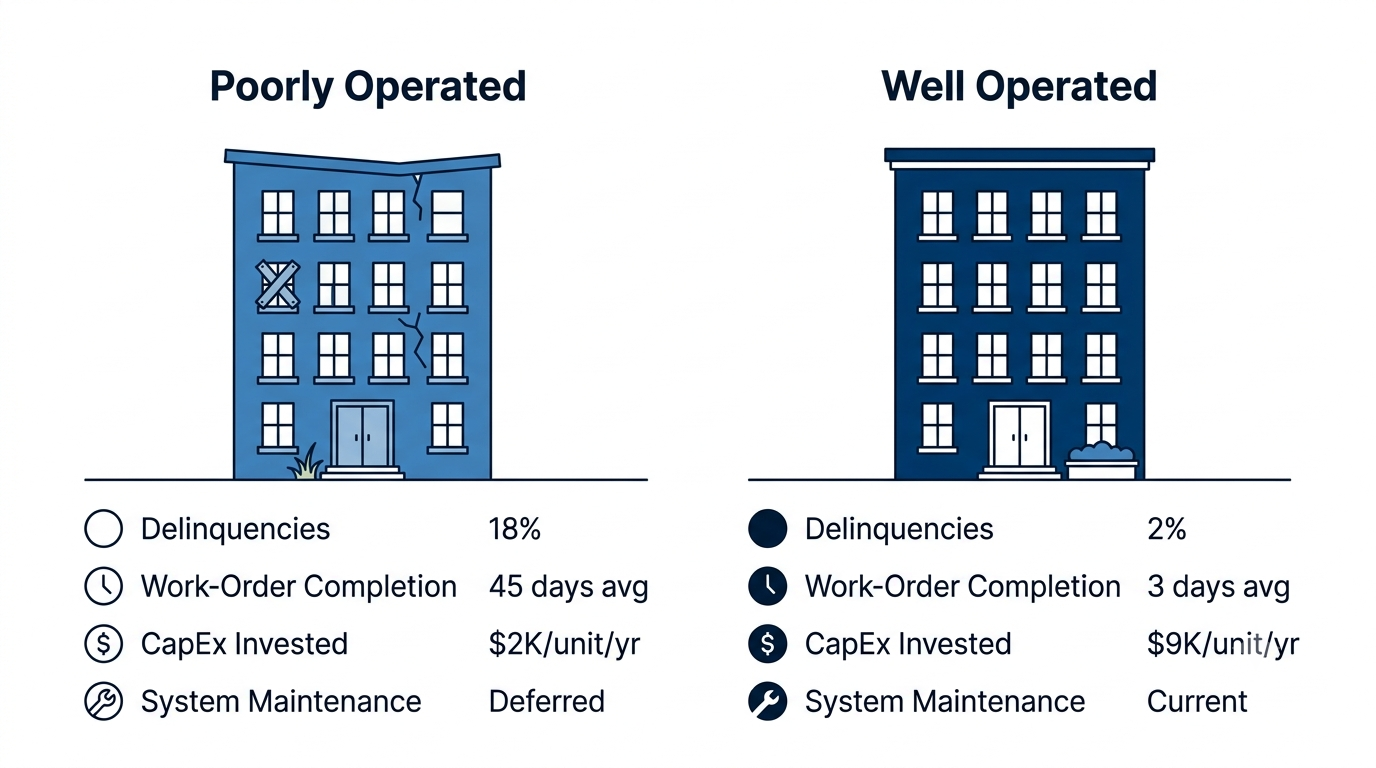

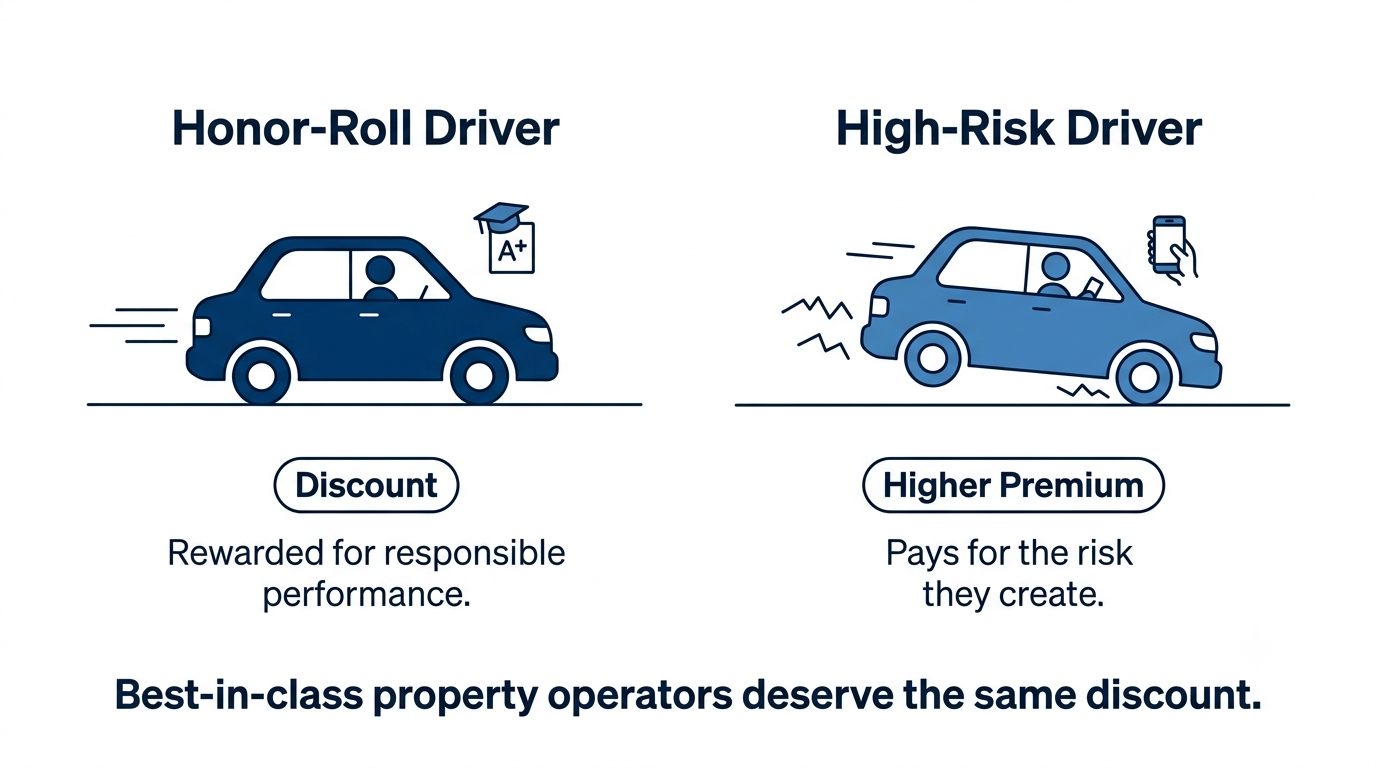

4. Operator Data: Under Development

RPC believes the property insurance industry should use operator-performance metrics to more accurately price coverage and predict risk. An operator performing in the top decile for low delinquencies, rapid work-order completion, and preventive maintenance may present a lower risk than a bottom-decile operator with similar buildings on paper. RPC believes its best-in-class operators deserve the same opportunity to turn operating quality into insurance savings.

Potential operator metrics

RPC plans to monitor more than 10 operator metrics from participating members' property-management systems and combine those indicators into a proprietary risk-index score, including:

- •Delinquency levels

- •Work-order response and completion times

- •Preventive maintenance

- •Capital expenditures on building systems

- •Inspection results

- •On-site supervision

- •Vacancy and turnover

- •Open safety issues

- •Claims frequency and severity

A Protected-Cell Captive, Purpose-Built for Property

RPC is a protected-cell captive platform purpose-built for property owners and operators, giving members access to captive ownership and economics through shared institutional infrastructure.

- •Each member's cell capital, underwriting results, and surplus are legally segregated

- •Member risk is insulated from unrelated participant liabilities, subject to the governing structure and policy terms

- •Premium funds individual and shared captive losses before applicable reinsurance responds

- •Members may be eligible for dividends from retained underwriting results and investment income

- •Shared infrastructure reduces the cost of captive management, actuarial work, audit, compliance, claims administration, and technology

Founded by an Owner, Not Just an Underwriter

Angad Guglani is a career real estate investor and founder of Cooper Square Acquisitions. Starting in 2016, he built a $60M portfolio with no institutional sponsorship, running it in-house down to acquisitions and property management, producing a loss history under 5% over the past decade.

Program & Reinsurance Structure

RPC is a fronted insurance program. Members receive fully binding property insurance policies issued by AIG Lexington, with the agreed captive layer reinsured back to RPC and additional risk transferred through the program's reinsurance tower.

Policy Issued

The member receives an AIG Lexington insurance policy and premium is paid into the fronted program.

Captive Layer Reinsured

The agreed retained layer is reinsured to RPC, which funds covered losses within its retained layer.

Panel Responds

The reinsurance panel of up to 20 global A-rated reinsurers responds above the captive retention.

Carrier Pays Claims

The fronting carrier remains the policy issuer and claims-paying counterparty to the insured.

Day-to-Day Operations & Lender Compliance

Members manage their policies and portfolios through the RPC portal, with policy questions addressed through RPC's partnership with Atlas Partners, an independent risk advisor with more than 40 years of experience. AIG Lexington remains the issuing carrier, and members, lenders, and limited partners receive the same type of carrier-issued evidence of insurance expected in a conventional placement.

Policy & portfolio management

- •Add and remove properties through the portal

- •Maintain schedules of values and portfolio information

- •Request and manage insurance certificates

- •Add additional insureds where permitted

- •Review policy and program documents

- •Track submissions, changes, and outstanding requirements

Compliance framework

- •Carrier-issued policy and certificates of insurance

- •Ability to identify lenders as additional insureds or loss payees where applicable

- •Program review by the issuing carrier, plus reinsurance and counterparty review

- •Annual regulation and reporting in the captive's domicile

- •Licensed and insured captive service providers

- •Audited financial statements and actuarial oversight

Risks & Mitigants

The captive structure introduces member participation in retained underwriting risk, defined and limited through collateral, aggregate retention, reinsurance, governance, and regulatory oversight.

Captive Team

RPC coordinates a full team of licensed and specialized service providers, so members do not need to assemble or supervise a fragmented captive operating stack.

Certified Public Accountant

Prepares and audits financial statements required for management, members, and regulatory filings.

Legal Counsel

Advises on policy language, captive structure, contracts, governance, and insurance regulation.

Licensed Actuary & Property Underwriter

Supports member underwriting, exposure analysis, loss projections, rating, collateral, and captive funding requirements.

Licensed Captive Manager

Provides monthly accounting, vendor coordination, financial reporting, domicile communication, and regulatory filings.

Reinsurance Brokers

Structure and place the reinsurance tower while maintaining relationships with the program's 15-plus reinsurance partners.

Third-Party Claims Administrator

Provides licensed claims administration, including intake, investigation, reserving, valuation, and settlement support.

Investment Manager

Invests captive assets within approved regulatory and governance constraints to support captive economics and potential distributions.

Insurance Portal Provider

Lets members add and remove properties, maintain portfolio information, request documents, and manage policy activity.

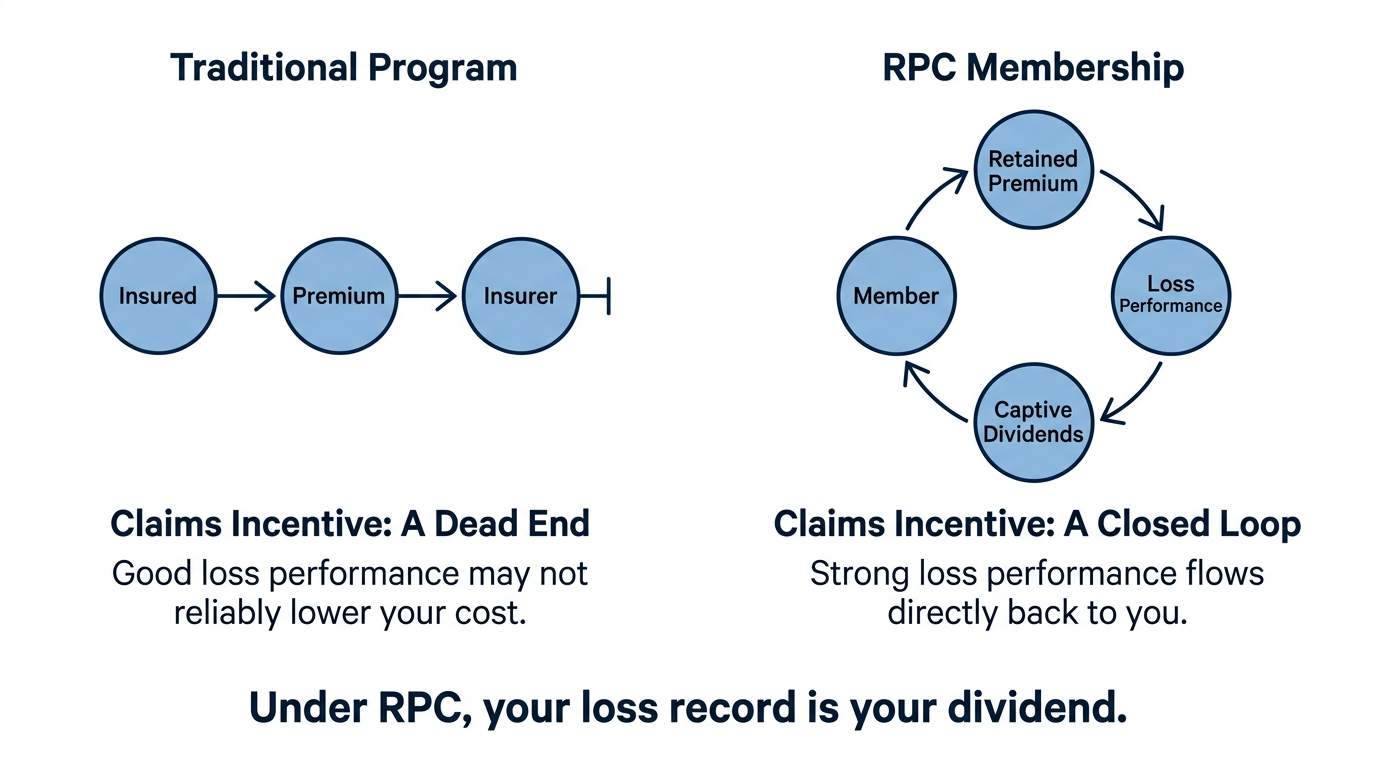

Claims Handling

Claims are handled through a licensed third-party claims administrator operating under the authority of the fronting carrier and the captive program. Because members participate in the captive's underwriting results, RPC has a direct interest in accurate reserving, efficient claim resolution, and avoidance of unnecessary claim leakage, while claims are paid fairly under the policy.

Investment Management

RPC's objective is to dividend excess funds back to members as soon as prudently and legally available. While funds remain within the captive, the investment manager invests premium and collateral assets in conservative, income-producing instruments permitted by insurance regulation, helping offset program expenses and strengthen surplus.

Eligibility Requirements

If easier, members may forward the same portfolio information previously provided to their existing insurance broker, and RPC's intake team will organize the submission and coordinate underwriting.

Who RPC is designed for

- •Property owners and operators with meaningful annual insurance premium

- •Portfolios requiring lender-compliant, fronted insurance policies

- •Operators with strong historical loss performance, generally a sub-25% loss ratio

- •Members willing to contribute collateral and retain risk through the captive

- •Owners seeking long-term control, transparency, and participation in underwriting economics

Initial underwriting information

- •Current schedule of values or rent roll

- •Five-year loss runs

- •Current insurance policies and endorsements

- •Property-level construction, occupancy, protection, and exposure information

- •Current premium, deductible, limits, and lender requirements

- •Any catastrophe modeling, replacement-cost estimates, or engineering information available

Ready to Own Your Insurance?

Be among the first to join Real Property Captive and transform your insurance spend into owned equity. Our protected cell structure is designed to make captive insurance accessible to mid-sized real estate owners.